Data Readiness for AI in Credit Card Portfolio Management: The Foundation for Transformation

A Comprehensive Guide to AI Data Readiness for Credit Card Issuers

_______________________________________________________________________________________

Editor's Note:

This article is Part 1 of our series on "AI in Portfolio Management: From Theory to Action" in which we explore how AI is reshaping Credit Card and Payment Portfolios beyond traditional segmentation and predictive models.

In this first part, we explore how structured, cleaned, and enriched data forms the backbone of AI-driven credit card portfolio management, enabling accurate insights, fraud detection, and personalized customer engagement.

Coming up next: AI-Powered Growth: Scaling Credit Card Portfolios with Intelligence

Stay tuned and follow us for more insights!

__________________________________________________________________________________________

(Continuing our series on AI Readiness for Credit Card Issuers)

Introduction: In our series opening blog, AI and Portfolio Management: Why Now?, we explored how embracing AI is not a question of why but when! We also learned from examples that American Express uses IBM Watson for early churn and dormancy and that Capital One is leveraging OpenAI for spending and rewards optimization. While these almost Jarvis-inspired use cases are definitely where the industry is headed, the journey of transformation however starts with data readiness.

Today, we’re delving deeper into the question of why the "AI promise" is often unfulfilled. The answer isn't poor technology—it’s inadequate data.

When banks and fintechs talk about artificial intelligence (AI), you might picture smart apps, instant fraud alerts, or personalized financial insights. These services promise a powerful new experience—but there's a hidden issue limiting AI’s potential: fragmented, messy, and disconnected data.

Capital One surveyed 4,000 business leaders and technical practitioners to assess AI data readiness across industries. The survey found a surprising gap between perceived AI readiness and the reality of operational challenges.

Here are some key findings of the Capital One AI readiness survey

Overconfidence vs. reality: 87% of business leaders see their data ecosystem as ready to build and deploy AI at scale, yet 70% of technical practitioners spend hours daily fixing data issues.

Data culture disconnect: Leaders say data culture is a top indicator of AI success, but only 35% of respondents say they have a strong data culture, citing inconsistent support and education.

Strategy misalignment: While 78% of tech practitioners and 82% of leaders agree on the importance of an AI strategy, only 53% of tech practitioners and 55% of leaders are fully familiar with their business’ AI strategy.

Source: https://www.capitalone.com/tech/machine-learning/ai-readiness-survey/

Here’s what you should consider to get ready for Artificial Intelligence

AI is Only as Smart as Its Data:

Imagine cooking a gourmet meal using expired ingredients. No matter how skilled the chef is, the meal won’t taste good. Similarly, no matter how advanced an AI model is, if the underlying data isn't timely, accurate, and complete, the results will disappoint.

As a credit card issuer, evaluate how smart your data ecosystem using the following questions:

What % of your data resides on cloud-native environments like AWS, Google vertex AI, or Azure

How many processes in your organization fire event-driven data pipelines (Kafka, Snowflake)?

Do you have a cross-product unified view of the consumer (Credit Cards, Loans, Deposits)?

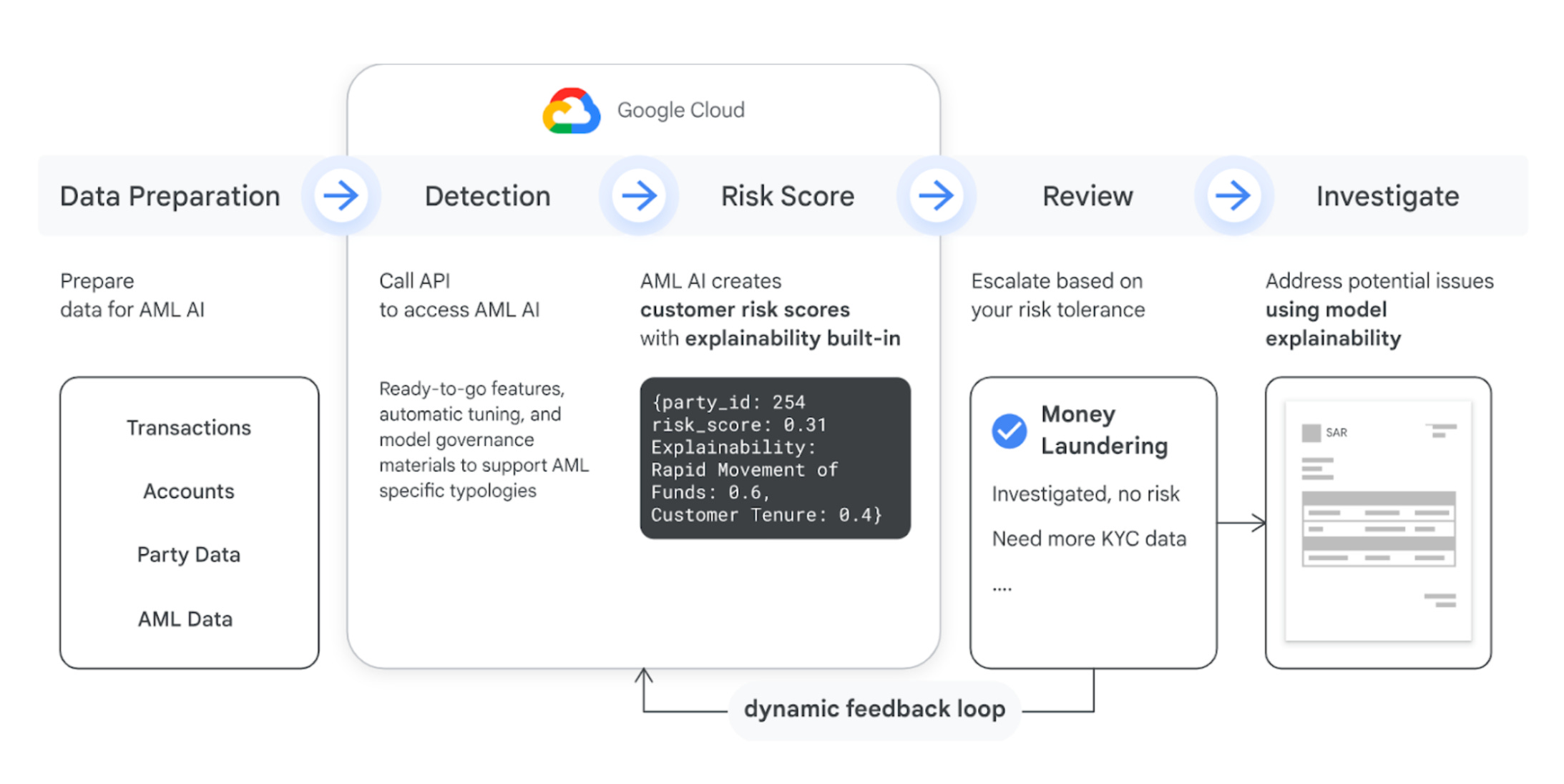

Example: HSBC partnered with Google Cloud to develop and implement an AI solution capable of recognizing suspicious activity on its own without us telling it what to look for. Using Google’s extensive knowledge of money laundering in its many forms, it trained Anti-Money Laundering AI (AML AI) on HSBC’s vast customer data to spot suspicious activity with more precision than manual optimization.

Google Cloud AML AI Architecture:

Source: https://cloud.google.com/financial-services/anti-money-laundering/docs/concepts/overview

Legacy Systems: The Big Bank Barrier

Most traditional banks still rely on legacy IT systems designed decades ago, updating information overnight instead of in real-time. AI, however, thrives on instant access to the latest data. This gap severely restricts AI’s effectiveness in critical areas like fraud detection and real-time credit decisions.

In contrast, global leaders like JP Morgan Chase and Visa have proactively invested billions in modern cloud infrastructure. This has allowed them to process transactions and update AI models in real-time, dramatically improving speed and accuracy.

Data Silos: AI’s Blind Spots

Have you ever wondered why different departments within your bank don't seem to communicate? The reality is, that customer data is often fragmented across different systems—transactions, marketing interactions, customer support calls, and more. These data silos create significant blind spots, making it harder for AI to recognize patterns or deliver personalized insights.

For instance, if you report suspicious activity via chat, but the chat system isn't integrated with fraud monitoring, AI won't see the connection. The result? Delayed responses and missed opportunities to enhance customer security.

Governance is Not Optional

Credit card issuers face strict regulations globally, including GDPR in Europe, requiring transparency in AI decisions. Customers rightly expect to know why a credit limit was reduced or a transaction was flagged.

However many AI systems are "black boxes," making explainability challenging. Global institutions like ICICI Bank and HSBC have started to address this issue by developing frameworks for transparent AI decision-making, ensuring they comply with regulations while building customer trust.

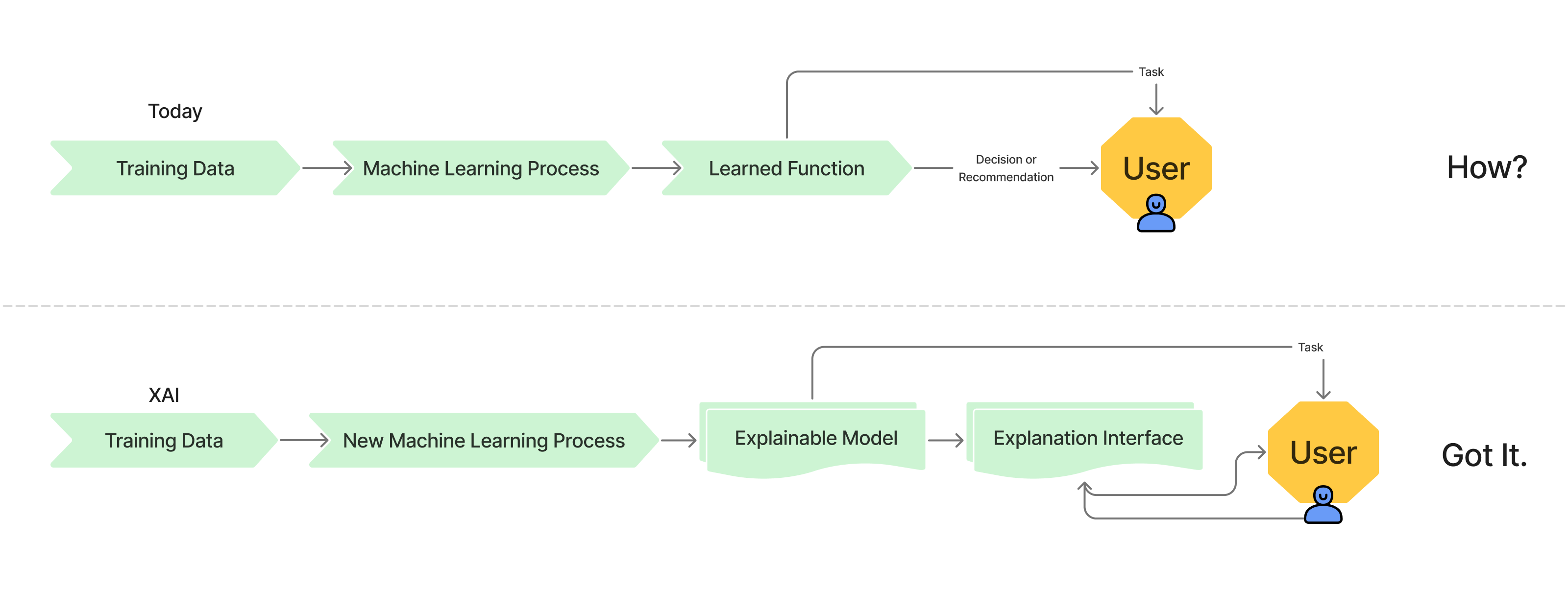

What is Explainable AI?

Explainable AI (XAI) is a field of study that allows AI systems to explain how they make decisions. This helps users understand how AI systems arrive at their conclusions. XAI is also known as transparent or interpretable AI.

To implement explainable AI (XAI) in Python, you can use one of the following approaches:

LIME (Local Interpretable Model-agnostic Explanations):– LIME is a popular XAI approach that uses a local approximation of the model to provide interpretable and explainable insights

SHAP (Shapley Additive exPlanations):– SHAP is an XAI approach that uses the Shapley value from game theory to provide interpretable and explainable insights

ELI5 (Explain Like I’m 5): The ELI5 framework simplifies complex ideas into easy-to-understand concepts using simple language, relatable examples, and minimal jargon, making them accessible to anyone.

Source: https://www.geeksforgeeks.org/explainable-artificial-intelligencexai/

Multi-Modal Data: The Next Frontier

Customers now interact across multiple channels—voice, chat, and even uploading images like receipts or IDs. Yet, banks frequently overlook these valuable data streams.

Imagine this scenario: You call your bank to dispute a transaction. An AI-driven system immediately transcribes your voice complaint, cross-checks your transaction history, and sends you an instant confirmation or a fraud alert. Some global fintechs and progressive banks are already piloting these multi-modal experiences, greatly enhancing customer satisfaction. Read Annexure 1 to understand the implementation of a Voice-Based Customer Dispute Resolution solution using multi-modal data.

Data Awareness at every level:

AI readiness isn’t just an IT function. Product teams play a critical role. Here’s how Different Roles Can Strengthen Data Readiness:

👩💻 Junior Product Managers:

Ensure app event tracking follows standardized nomenclature (e.g., transaction logs, authentication events).

Validate that every customer touchpoint logs usable data—from rewards opt-ins to declined transactions.

👨💼 Senior Product Managers:

Ensure all systems are logging customer interactions, including outsourced services.

Drive app journey mapping so AI models have full visibility into user behavior.

Unified Data: Unlocking AI’s Full Potential

What if banks combined all data—transactions, chats, voice interactions—into a single view? The result would revolutionize customer experience:

Instant Fraud Detection: AI can identify unusual behavior the moment it happens.

Personalized Credit Management: Real-time adjustments to credit limits based on immediate financial data.

Proactive Insights: AI-driven reminders based on actual spending patterns—"You usually pay your bill today; here's a reminder to avoid late fees."

Capital One’s "Eno" chatbot exemplifies this potential. Leveraging real-time, unified data, Eno provides personalized, timely advice and enhances customer interactions significantly.

Key Takeaways :

If credit card issuers want to truly leverage AI, they need to treat data readiness as a strategic priority—not an afterthought.

Invest in modern cloud data infrastructure for AI scalability.

Establish strong data governance and AI accountability frameworks.

Fix data quality issues before AI models train on them.

Ensure regulatory alignment—AI compliance is just as important as AI accuracy.

What’s Next in the Series?

With this, we conclude our Part 1 of the series: AI in Portfolio Management: Foundation.

🔜 Coming up next:

📌 AI Impact in Growth Functions—How AI is reshaping cardholder activation, spend growth, and retention.

📌 Lifecycle Management with AI—How issuers are using AI to personalize engagement at every customer touchpoint.

📌 AI for Credit Line Management—The evolution of dynamic credit decisions.

Assess your AI data readiness with Yield Lab. Connect with us for a hands-on strategy session.

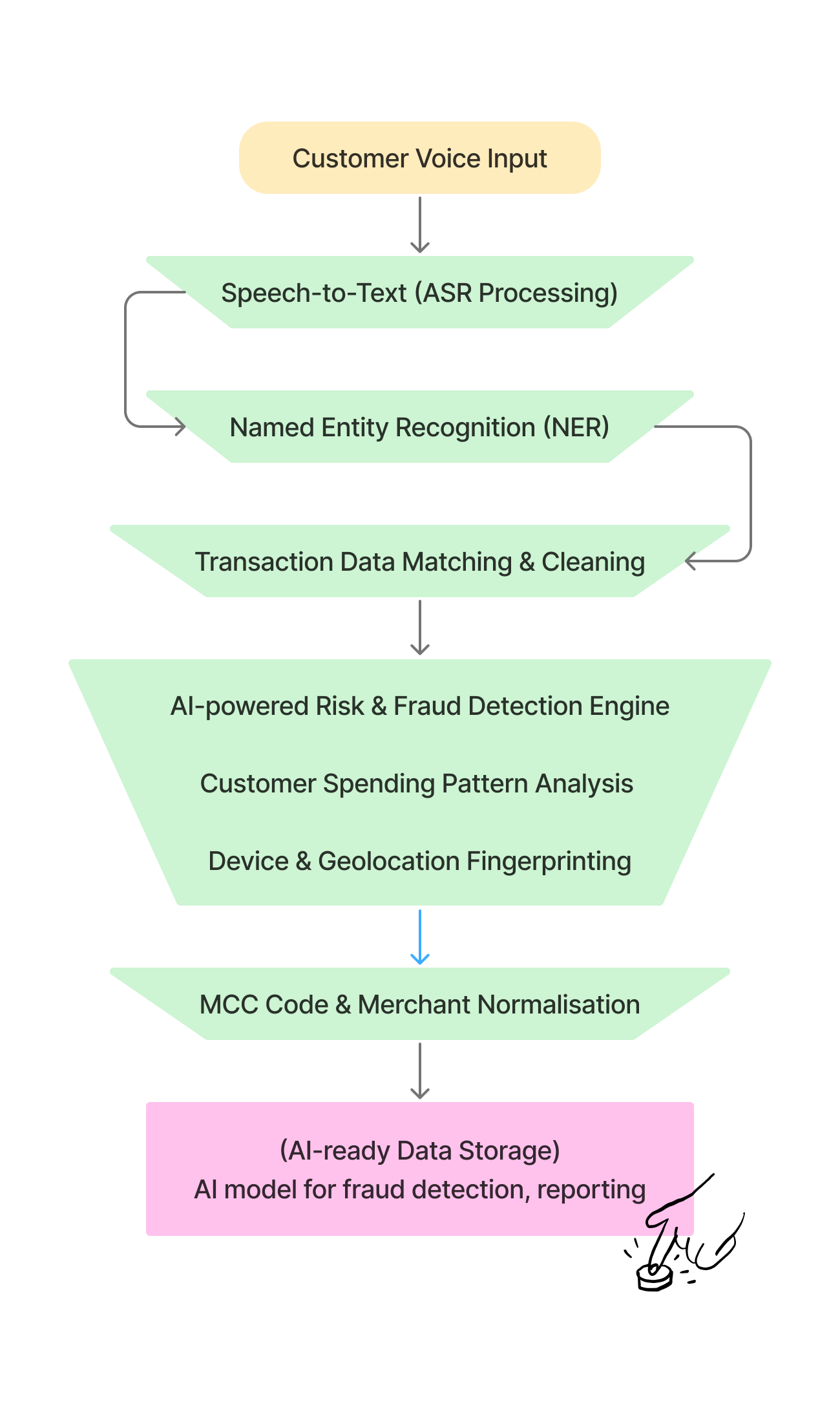

Annexure 1: Implementing Voice-Based Customer Dispute Resolution using Multi-modal data framework

Modern AI-driven banking solutions allow customers to dispute transactions via voice commands on WhatsApp, IVR, or a mobile banking app. However, voice data is unstructured and requires multiple stages of cleaning and enrichment before storing it for AI-driven analysis.

Step 1: Raw Voice Input (Customer Call to Dispute a Transaction)

A customer calls the bank's AI-powered assistant and says:

🔊 "Hey, I see a charge of ₹3,499 from ‘XYZ Merchant’ on my credit card. I don't recognize this. Can you check?"

The system captures this voice data as an audio file.

Step 2: Data Cleaning & Processing Pipeline

The following transformations take place:

Speech-to-Text Conversion (ASR - Automatic Speech Recognition)

Converts voice input into text:

"Hey, I see a charge of 3499 rupees from XYZ Merchant on my credit card. I don't recognize this. Can you check?"

Named Entity Recognition (NER) for Key Data Extraction

AI models extract structured fields from unstructured speech:

Transaction Amount - ₹3,499

Merchant Name - XYZ Merchant

Action Requested - Dispute Transaction

Matching with Transaction Data

We now compare the extracted details with the actual credit card transaction records:

Transaction ID - TXN12034

Amount - ₹3,499

Merchant Name - XYZ Ecom India

Location - Delhi

MCC Code - 5732

Timestamp - 2025-03-15 12:45:00

Issue: The system detects a merchant name mismatch ("XYZ Merchant" vs "XYZ Ecom India").

Solution:

Use Merchant Category Code (MCC) 5732 (Electronics Store) for normalization.

Check for alternative names (XYZ, XYZ Ecom, XYZ India) in our database.

Validate whether the customer has shopped at XYZ before.

AI-powered Decisioning: Is This a Fraudulent Transaction?

Once the cleaned data is structured, AI models analyze the customer’s historical transactions with XYZ.

Device fingerprinting (Was the transaction from their usual phone/laptop?).

Geolocation patterns (Was it done from an unexpected location?).

If AI predicts potential fraud (80% confidence), it triggers:

Instant temporary card block.

The customer gets a push notification: 📲 "Suspicious Transaction Detected: ₹3,499 at XYZ. Confirm if this was you."

Step 3: Storing Cleaned Data for AI & Reporting

The cleaned and structured data is stored in an AI-ready fraud detection database:

Transaction ID - TXN12034

Amount - ₹3,499

Merchant Name - XYZ Ecom India

MCC Code - 5732

Timestamp - 2025-03-15 12:45:00

Customer History - First time purchased

Risk Score - 80%

Action Taken - Card blocked temporarily

Below is a technical architecture showing how voice and transaction data are cleaned and structured for AI: