The Story of Petal Card and How It Implemented Machine Learning to Underwrite 4 Million Cards

What Petal Card’s CashScore Can Teach India’s Fintech Ecosystem

Editor’s Note

As we continue exploring real-world use cases of AI in driving growth, this time we dive into the journey of Petal Card — a US-based credit card issuer that not only leveraged Machine Learning to underwrite bureau-thin customers but also built something powerful enough to become a stand-alone product used across the industry.

Reimagining Credit Underwriting in a Data-Driven World

Financial institutions have long been at the forefront of underwriting innovation, largely because they were among the earliest industries to digitize customer data. Today, nearly every credit card issuer around the world uses some form of Machine Learning in their underwriting processes. However, there remains a core issue: most of this underwriting still relies on a lagging indicator — the credit bureau score.

Typically updated once every 30 days, bureau scores often fail to reflect a customer’s current financial situation. This heavy reliance on outdated bureau data leads most institutions to chase after the same segment of bureau-thick customers, leaving little room to grow the market or serve new segments. While many fintechs and banks have begun exploring alternative data sources, few have managed to scale a model that can reliably and compliantly underwrite at volume.

This is why Petal Card’s story stands out — not just for its innovative use of data, but because it started with a clear mission: to play the game fairly and expand access to credit for those often overlooked.

The Petal Card Journey

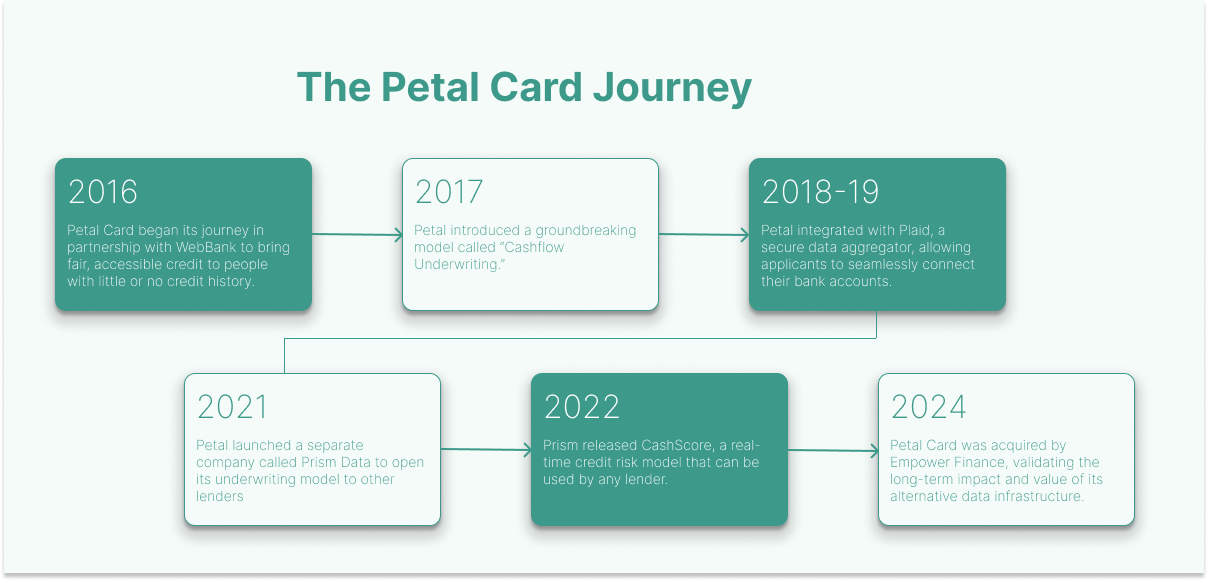

Founded in 2016 by American entrepreneur Jason Gross, Petal Card began its journey in partnership with WebBank to bring fair, accessible credit to people with little or no credit history.

September 2017: Petal introduced a groundbreaking model it called “Cashflow Underwriting.” Rather than relying solely on credit scores, it built a proprietary model that analyzed an individual's real-time financial behavior, such as how much they earn, how regularly they pay bills, and how consistently they manage their spending.

2018–2019: Petal integrated with Plaid, a secure data aggregator, allowing applicants to seamlessly connect their bank accounts. This allowed Petal to collect banking data on the fly and underwrite more effectively — a concept remarkably similar to India’s Account Aggregator ecosystem under Sahamati.

April 2021: Amidst the global COVID crisis, Petal launched a separate company called Prism Data to make its underwriting model available to other financial institutions, especially those trying to better serve bureau-thin or credit-invisible customers.

October 2022: Prism released CashScore, a real-time credit risk model that can be used by any lender. CashScore® leverages thousands of financial data points typically missing from credit bureau reports — including income, expenses, financial volatility, and a user’s ability to pay.

2024: Petal Card was acquired by Empower Finance, validating the long-term impact and value of its alternative data infrastructure.

How Petal Card Built the CashScore Engine

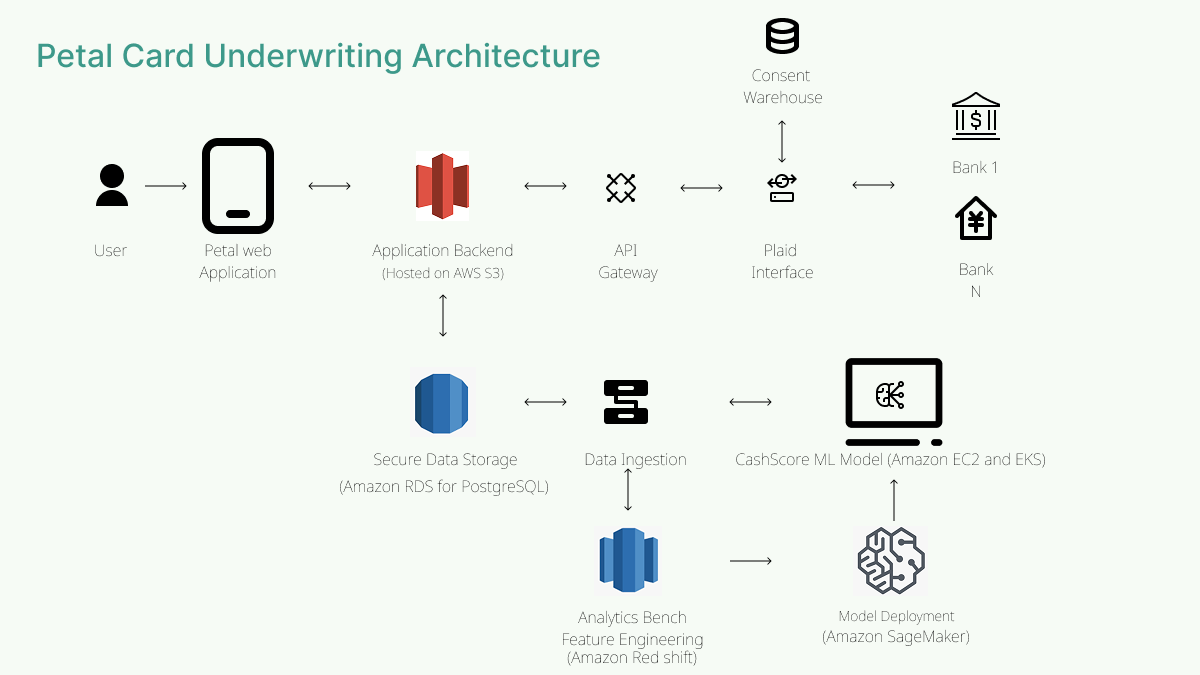

Petal’s entire tech stack is built on top of Amazon Web Services (AWS) — supporting everything from backend services to front-end user experiences. Here’s how the full system comes together:

Frontend Hosting: Customers begin their journey through a Petal web application. The UI is hosted via Amazon S3, known for its high scalability, availability, and performance.

Core Data Storage: Transactional business data is stored in Amazon RDS (PostgreSQL), while analytical and research data is housed in Amazon Redshift and S3.

Machine Learning Infrastructure: Data flows into Petal’s proprietary ML models, which are trained and deployed using Amazon SageMaker — AWS’s fully managed ML platform that handles everything from training to deployment.

Compute Needs: For scalable compute resources, Petal runs its services on Amazon EC2, and for containerized workloads, it uses Amazon EKS to manage Kubernetes clusters efficiently.

This cloud-native setup allowed Petal to move fast, scale easily, and securely manage the complex data infrastructure required for machine learning–based underwriting.

Key Features Used in Cashflow Underwriting

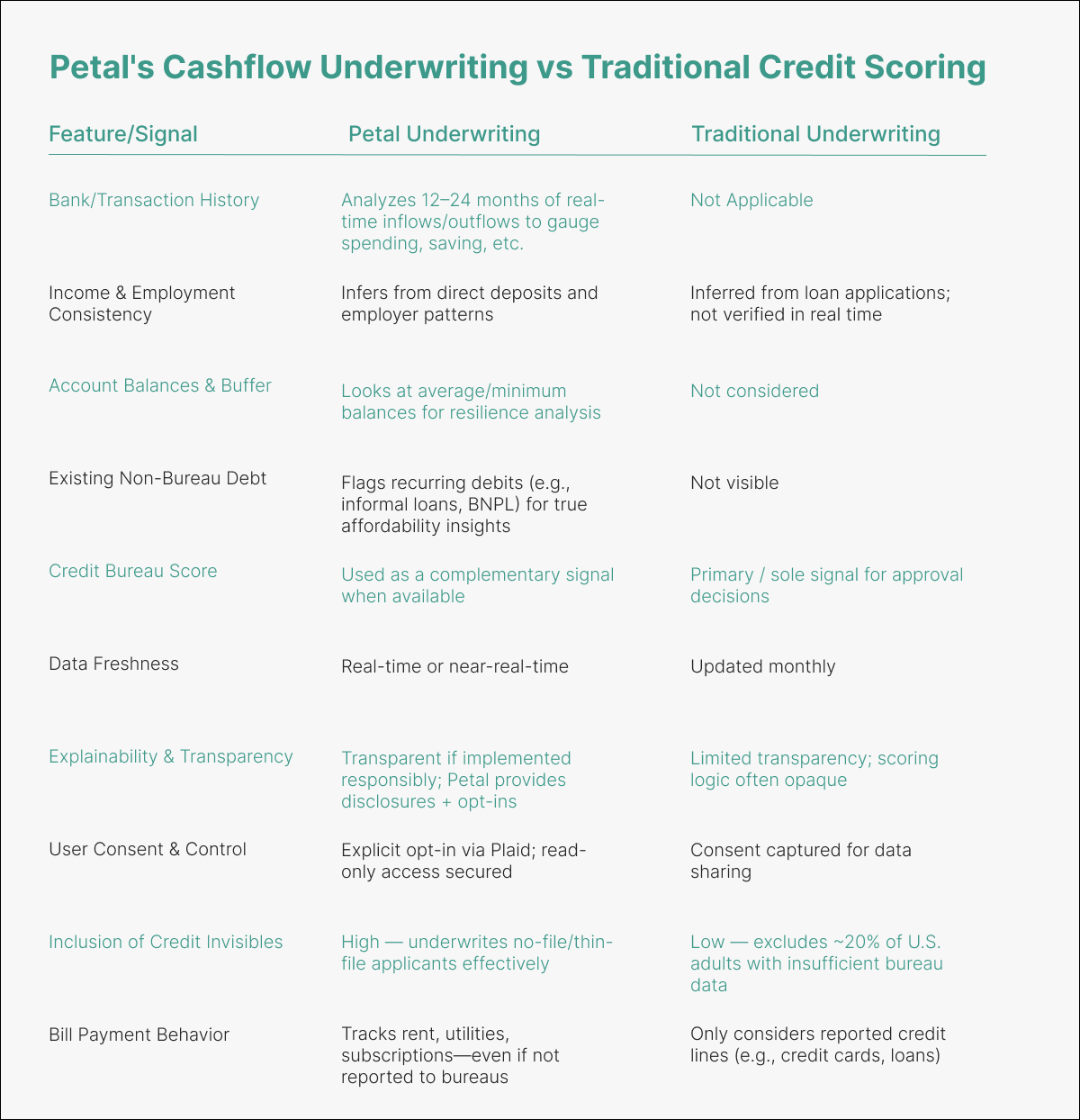

Petal’s model doesn’t just look at one or two signals — it builds a multi-dimensional picture of the applicant’s financial life using several nuanced data points:

1. Bank Transaction History

Petal analyzes up to 24 months of checking and savings account activity to understand cash inflows and outflows. This data reveals income patterns (e.g., gig vs. salaried income), spending habits (essential vs. discretionary), and the applicant’s consistency in maintaining a balance — all of which provide more accurate credit insight than a static score.

2. Bill Payment Behavior

By analyzing recurring payments — such as rent, utilities, or mobile bills — Petal evaluates whether the applicant reliably meets their financial obligations, even if these aren’t reported to credit bureaus. Missed payments or overdrafts are likely flagged as stress indicators.

3. Income and Employment Validation

Recurring direct deposits are used to infer employment status, employer identity, and salary stability. Prism Data (Petal’s platform) even analyzes income volatility — offering lenders a clearer sense of whether an applicant’s income is stable enough to sustain credit repayment.

4. Account Balances and Savings Buffer

The average and minimum balances maintained over time can tell a lot about an applicant’s financial resilience. Someone who consistently maintains even modest savings is statistically less likely to default.

5. Existing (Non-Bureau) Debt

Some applicants may already be repaying loans or obligations not captured in bureau reports — these show up as monthly outflows in the bank data. Petal uses this to calculate true affordability.

6. Credit Bureau Data

Petal doesn’t ignore bureau data — it uses it when available, but as a complementary source. If a FICO score is present, it’s incorporated alongside cashflow data. But for those without traditional credit files, cashflow becomes the primary indicator. Interestingly, Petal has found that combining both improves predictive accuracy.

How Petal Manages Risk and Privacy While Handling Banking Data

Handling sensitive banking data comes with significant privacy risks — and Petal treats this responsibility with rigor. Here’s how:

Consumer Consent: The process begins with explicit user permission. Customers must actively opt-in to share banking data — and Petal is transparent about how that data will be used to improve their credit chances.

Secure Data Transmission: Plaid’s API ensures encrypted transmission (TLS/HTTPS). Petal never sees the customer’s login credentials — only a secure token that enables read-only access.

Data Minimization & Anonymization: After extracting features for modeling, raw data is minimized or compartmentalized. CashScore is trained on anonymized datasets to enhance security and privacy — even during product development or model refinement.

Access Control: Internal teams work with anonymized data wherever possible. Customer-facing systems display only the authenticated user’s data, and access to sensitive data is strictly permissioned.

Regulatory Compliance: Petal complies with GLBA, CCPA, and where applicable, the Fair Credit Reporting Act (FCRA). Adverse action notices are issued even when decisions are made using CashScore, ensuring transparency.

Navigating the Regulatory Landscape

Cashflow underwriting is gaining regulatory support in the U.S., and Petal is at the center of this shift.

2019: A joint statement from five federal agencies (CFPB, OCC, FDIC, Federal Reserve, NCUA) encouraged the use of alternative data like cashflow, calling it a lower-risk and more inclusive alternative to traditional methods.

Fair Lending Compliance (ECOA): Petal proactively runs fair-lending tests on its models to ensure that decisions aren’t skewed against protected classes. The variables used (like income and expenses) have strong business justifications, reducing bias risk.

FCRA and CRA Classification: While Petal itself isn’t a credit bureau, when Prism Data began offering CashScore to third parties, compliance became necessary. That’s why Plaid Check, now a CRA, ensures reports generated through Prism adhere to FCRA regulations.

Bank Oversight: Since WebBank is the official issuer of Petal cards, all models had to be reviewed and validated through WebBank’s compliance, credit risk, and regulatory teams.

Future of Open Banking: With Section 1033 of Dodd-Frank gaining momentum, the right for consumers to share their banking data will be further enshrined, making models like Petal’s even more viable at scale.

Strategic Insight: Why This Matters for India

Petal Card is a playbook-in-the-making for India’s fintechs.

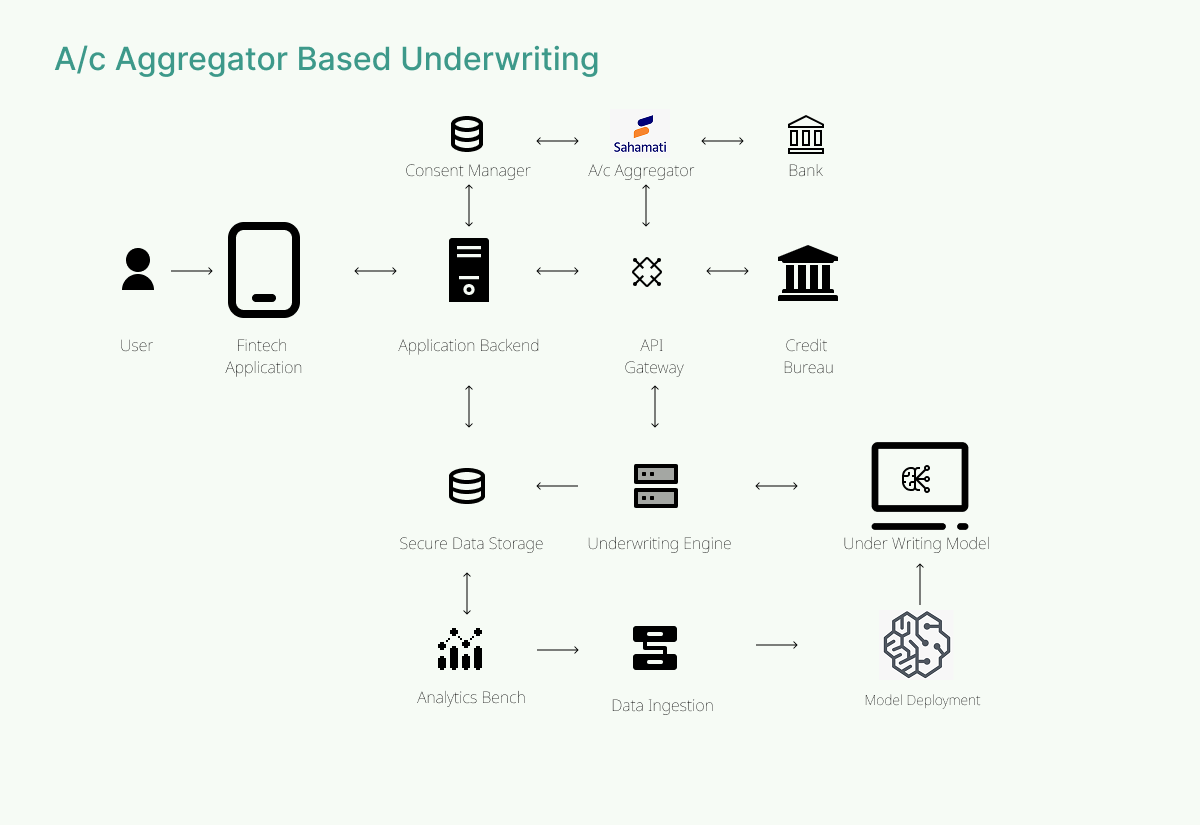

With nearly 200 billion UPI transactions a year and a fully operational Account Aggregator (AA) framework, India has already laid the digital rails for cashflow-based underwriting. The real challenge is cleaning and standardizing the data — but that’s where Gen AI comes in.

Named-entity recognition on merchant data, real-time enrichment of savings patterns, and processing of multi-modal signals (video KYC, call center transcripts, etc.) are now entirely possible with Generative AI. This opens the door to real-time, multi-variate underwriting models that go far beyond legacy scorecards.

Already, 10% of personal loans disbursed in India in December 2024 used AA-enabled data — a signal that this shift is underway.

Here’s a proposed architecture to implement A/c Aggregator-based underwriting:

Conclusion: The Leap from Machine Learning to Generative AI Has Begun

Petal’s journey shows how financial inclusion and cutting-edge ML models can go hand-in-hand when built responsibly, transparently, and with user permission at the core.

And now, India is ready for the next leap.

Just as Petal pioneered cashflow underwriting in the US, the Indian ecosystem is ripe to evolve from Machine Learning to Generative AI–based decision systems — systems that are real-time, personalized, and built on live behavioral data.

If you enjoyed this case study, let us know! Other fintechs like Kredivo, TomoCredit, and Upstart have also made major strides in this space. Let us know in the comments if you’d like a deep dive on them.

📌 Next in the Series: We’ll explore how AI is being used to manage credit line increases, with a real-world case study and architecture breakdown.

To receive early access, subscribe to YieldLabResearch.substack.com

🧠 AI Disclaimers:

Research powered by ChatGPT-4o

Grammar polishing done using Grammarly